Public sector defined benefit pension plans are intended to provide lifetime retirement income for employees. But in truth, too many defined benefit plan participants will never see a single penny of these pension annuity payments. The promise of payment at retirement is an illusion for most public employees because traditional “final average salary” defined benefit pension plans are designed to maximize benefits specifically for long-term employees, often to the detriment of employees who only stay in their jobs for a few years.

If the public policy goal for retirement plans is to allow as many individuals as possible to become financially self-sufficient, then public sector defined benefit (DB) plans are falling short and should be redesigned to use individual account features that exist in defined contribution (DC) and cash balance plans.

Traditional defined benefit pension plans have fundamental design weaknesses

Most traditional public sector plans calculate benefits based on a combination of the number of years of service, compensation, and a benefit accrual factor–e.g., 30 years of service x $50,000 compensation x 1.75% = $26,250 per year.

There is the added bonus that the benefit they accrue each year is not taxable during employment. Federal and state income taxes on this compensation are deferred until they actually retire and start receiving these annuity payments.

But this only works well for those who actually make a long career with a single public employer. What about workers who are short- and medium-tenure employees? These members simply do not significantly benefit from these defined benefit pension plans because: 1) they do not work long enough to vest in any pension benefit; and 2) even if they do vest, if they leave before retirement age, their benefit is frozen and loses value because of inflation and does not increase with any future pay increases (sometimes referred to as “the back-loading problem”).

Longer vesting requirements make the problem even worse for public pension plan participants

In the private sector, employer retirement plans are subject to federal laws under the Employees Retirement Income Security Act (ERISA), which dictates that a defined benefit plan cannot have a vesting requirement that is longer than five years of service (called cliff vesting) or a graduated vesting schedule longer than three to seven years of employment.

For an ERISA cash balance pension plan (another type of defined benefit retirement option), employees must vest in employer contributions no later than after three years. These ERISA minimum vesting rules were adopted, in part, as a response to company pension failures and to protect the benefits that were promised to plan participants. That public policy purpose remains valid today.

However, public employee pension plans are not subject to these ERISA minimum vesting and other requirements. This means public pension plans can and often do have much longer vesting requirements. A 2022 report by the Equable Institute evaluated the vesting periods for state retirement programs and found that of the examined 43 states with DB pensions, only 15 had an average vesting requirement of five years or less. The remaining 28 states had average vesting periods longer than five years. Seventeen states had vesting periods between five and 10 years, and 11 had average vesting periods of over 10 years. The report noted that of the 14 states with hybrid (combination DB and DC) plans, seven had vesting periods of five years or less and one had vesting longer than five years. In contrast, none of the 13 states that offer DC plans for employees had vesting requirements longer than five years.

A 2012 report from the Center for Retirement Research at Boston College (CRR) determined that long vesting periods mean 47.6% of workers depart without any promise of future benefits. The report finds that an additional 18.6% of workers vest but leave covered employment before full retirement age with a deferred vested benefit. These deferred pension benefits are subject to lost value due to inflationary impacts until the employees retire. This means only about 35% of government-hired employees actually earn a pension that is not forfeited or significantly reduced in value by inflation.

Figure 1 below shows how inflation can substantially reduce the value of deferred vested pension benefits.

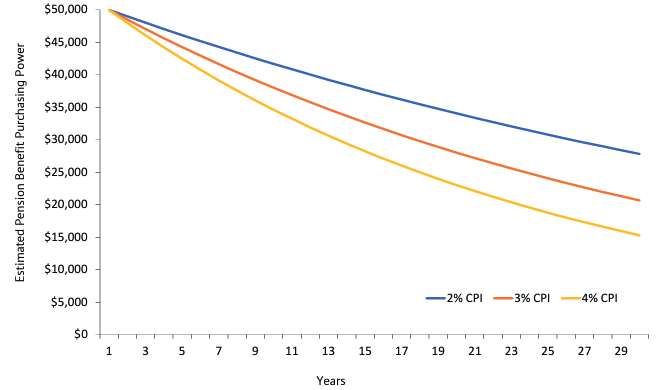

Figure 1: Impact of inflation on the purchasing power of pension benefits

Source: Reason Foundation paper “Best Practices for COLA Designs in Public Pension Systems”

Based on this analysis, almost two-thirds (65.1%) of states have vesting requirements that would violate the minimum vesting rules of ERISA for private sector plans. The CRR report notes that a 10-year vesting requirement reduces the probability of public employees earning full pension benefits by 16% compared to an ERISA-compliant five-year provision.

A 2021 Social Security Bulletin also confirmed the long vesting periods for many public pension plans, reporting a mean vesting period (all occupations) of eight years for the public plans examined, with a median of seven years. The mean vesting requirements for public safety employees was even longer at 9.2 years, with a median of 10 years. Many public safety pension plans (local plans in particular) even have vesting requirements as long as 20 years.

Unfortunately, some public pension financial reform efforts have made the vesting problem worse by making employees work even longer to take part in their retirement plan benefits. A 2018 National Association of State Retirement Administrators Issue Brief reported that nine states had increased vesting requirements from five to 10 years since 2009. Two states, Missouri and North Carolina, reversed the changes after further evaluation.

Individual account defined contribution and cash balance plans can provide better retirement security for more public employees

According to recent Bureau of Labor Statistics reports, state and local government employers spend, on average, 13.3% of their total compensation package on retirement benefits. Longer vesting means nearly half of workers who choose to work for public-sector employees will only be paid about 87% of their total compensation package. They will forfeit the rest. This is a fundamental problem for traditional DB pension plans that must be addressed by policymakers if the goal is to help as many as possible be self-sufficient in retirement, rather than relying on government welfare programs.

The previously mentioned Center for Retirement Research at Boston College report's conclusion states the problem very clearly:

“Sole reliance on final earnings defined benefit plans raises human resource and equity issues. Final earnings plans produce strongly back-loaded benefits and, when combined with delayed vesting, deprive short-term employees of retirement protection, especially for those systems that do not participate in Social Security.”

Individual account plan designs, including defined contribution and cash balance plans, avoid the fundamental problems of traditional DB plans by allowing full portability of benefits, protection against inflation, and more uniform benefit accruals. Where traditional DB pensions are still valuable, such should be part of hybrid DB/DC designs to mitigate the design shortcomings of a straight DB approach.

Short or immediate vesting can substantially reduce the forfeiture problem and provide a much-needed contribution to the retirement security of this large cohort of public employees who currently receive no significant benefits from traditional defined benefit pension plans.

State and local governments should not continue to support traditional defined benefit-only retirement programs with long vesting periods to the detriment of the retirement security of the many workers who will not make public employment a full career.

Stay in Touch with Our Pension Experts

Reason Foundation’s Pension Integrity Project has helped policymakers in states like Arizona, Colorado, Michigan, and Montana implement substantive pension reforms. Our monthly newsletter highlights the latest actuarial analysis and policy insights from our team.